Introduction

When a loved one dies, families face an overwhelming mix of grief and financial decisions — often simultaneously. Funeral arrangements need to be made within days. Bills don't pause. And if no coverage was in place, the costs can hit hard and fast.

The wrong type of coverage — or no coverage at all — can leave families scrambling at the worst possible moment.

Both policy types can help with end-of-life costs, but they serve very different purposes. Final expense insurance is a small permanent policy built specifically for funeral and burial expenses. Traditional life insurance covers a much broader range of financial needs — income replacement, debt payoff, legacy building.

According to LIMRA's 2025 Insurance Barometer study, 60% of consumers cite covering burial and final expenses as a reason for owning life insurance — yet 40% of adults (nearly 100 million people) say they need more coverage than they currently have.

What follows breaks down exactly how these two policy types differ — and how to determine which one actually fits your situation.

Key Takeaways

- Final expense insurance offers $5,000–$40,000 in permanent coverage with no medical exam, designed specifically for funeral and burial costs

- Traditional life insurance provides $50,000 to $1M+ in coverage for income replacement, debt payoff, and legacy planning

- Final expense insurance is easier to qualify for — especially for seniors and those with pre-existing conditions

- Holding both policies is a smart move for many: traditional life insurance for income protection, final expense for guaranteed funeral funds

- Final expense premiums are fixed for life — typically $30–$66/month based on age and coverage amount

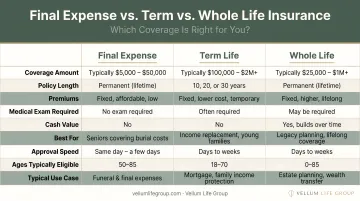

Final Expense vs. Life Insurance: Quick Comparison

| Feature | Final Expense Insurance | Term Life Insurance | Whole Life Insurance |

|---|---|---|---|

| Coverage Amount | $5,000–$40,000 (some carriers to $50,000) | $100,000–$1M+ | $50,000–$500,000+ |

| Coverage Duration | Lifetime (permanent) | 10, 20, or 30 years | Lifetime (permanent) |

| Medical Requirements | No exam; simplified or guaranteed issue | Medical exam often required | Medical exam often required |

| Typical Monthly Premium | $30–$66/month (age 50–65) | $35–$215/month (varies by age/coverage) | Higher; varies by age and coverage |

| Primary Purpose | Funeral, burial, end-of-life costs | Income replacement, debt payoff | Long-term protection + cash value |

| Typical Applicant Age | 50–85 | 25–55 | Any age |

| Cash Value | Minimal | None | Yes — tax-deferred growth |

Both product types fall under the life insurance umbrella, but they solve different problems. Final expense insurance is designed for one specific job — covering end-of-life costs so family members aren't left scrambling. Term and whole life policies are built around income replacement, long-term debt, and multi-decade financial protection.

On cash value: Term life builds none. Final expense insurance, structured as a small whole life policy, does accumulate cash value — but at typical coverage amounts of $10,000–$25,000, that growth is negligible compared to a traditional whole life policy designed for wealth transfer.

What Is Final Expense Insurance?

Final expense insurance is a type of small permanent life insurance designed specifically to cover end-of-life costs — funeral services, burial or cremation, outstanding medical bills, and related immediate expenses.

Coverage Amounts and Real-World Costs

Most policies cover $5,000 to $40,000, with some carriers offering up to $50,000. These figures aren't arbitrary. The National Funeral Directors Association reports the 2023 national median cost of a funeral with viewing and burial at $8,300, and a funeral with cremation at $6,280. Funeral expense costs rose 3.4% year over year as of May 2026 (BLS CPI data), so the case for locking in fixed premiums now is straightforward.

The Application Process

Most final expense policies don't require a medical exam. Instead, applicants answer a short health questionnaire — this is called simplified issue underwriting. Some policies go further with guaranteed issue underwriting, meaning no health questions at all, just age and residency requirements.

This accessibility defines the product's appeal for seniors and those with chronic health conditions who might not qualify for traditional life insurance.

The Graded Death Benefit — Know Before You Buy

Some final expense policies include a graded death benefit, meaning the full payout isn't available immediately after purchase.

- Gerber and State Farm guaranteed issue policies use a 2-year graded period for natural death

- Fidelity Life guaranteed issue uses a 3-year graded benefit period

- During this window, beneficiaries typically receive a return of premiums plus interest rather than the full death benefit

Simplified issue policies (where health questions are asked) often have no waiting period. If avoiding a waiting period matters to you, confirm this specifically before purchasing.

Premiums and Permanence

Premiums are fixed for life — they don't increase as you age or if your health changes. As long as premiums are paid, coverage never expires. For people on fixed incomes, that stability removes one variable from an already tight budget.

Use Cases for Final Expense Insurance

Final expense insurance fits a specific profile:

- Adults aged 50–85, especially seniors on fixed incomes

- Individuals with pre-existing health conditions who can't qualify for traditional policies

- People whose main concern is not burdening their family with funeral costs — not income replacement

- Those who no longer need large coverage (mortgage is paid off, children are grown) but want something in place for immediate end-of-life expenses

What Is Life Insurance?

Traditional life insurance is a broader financial protection product with two primary forms: term life (coverage for a defined period) and whole life (permanent coverage that builds cash value).

Coverage Amounts and Primary Uses

Traditional policies typically offer $50,000 to $1 million or more in coverage. The financial goals they address go well beyond funeral costs:

- Replacing a primary earner's income for surviving dependents

- Paying off a mortgage or other major debt

- Funding a child's education

- Covering specific financial obligations tied to income or assets

- Building a financial legacy

Health and Underwriting Requirements

Most traditional life insurance policies require either a full medical exam or a detailed health history submission. Premiums are tied directly to the applicant's age, health status, tobacco use, and lifestyle. According to the NAIC, traditional underwriting can include physical exams and fluid samples — though accelerated underwriting using data sources like prescription records and motor vehicle reports is increasingly available and can eliminate the in-person exam.

The younger and healthier you are when you apply, the lower your locked-in premium.

Whole Life's Cash Value Feature

Whole life insurance accumulates tax-deferred cash value over time — a feature neither term nor final expense policies include. A portion of each premium builds into a savings component that policyholders can borrow against or withdraw.

Outstanding loans reduce the death benefit, so this feature requires some management. But it adds a financial planning dimension worth considering for long-term coverage goals.

Use Cases for Traditional Life Insurance

Traditional life insurance is the right fit when:

- You are a primary earner with dependents relying on your income

- You carry significant debt — a mortgage, personal loans, or student loans

- You want to fund a child's education or leave a financial legacy

- You are in reasonably good health and can qualify at competitive rates

Term life works best for those who need high coverage during a defined period (while raising children or paying down a mortgage). A healthy 30-year-old can often get $500,000 in term coverage for under $30 per month. Whole life suits those who want lifelong coverage with a savings component baked in.

Final Expense vs. Life Insurance: Which Is Right for You?

The right choice depends on your age, health, financial obligations, and what you want coverage to accomplish. Ask yourself these four questions:

- What's my primary goal? Cover funeral costs only, or replace income and protect dependents?

- What's my health status? Can I realistically pass a medical exam?

- What's my monthly budget for premiums?

- Do my beneficiaries have financial needs beyond end-of-life expenses?

Choose Final Expense Insurance If:

- You are 50 or older with health challenges

- You're on a fixed income and need predictable, affordable premiums

- Your family's primary concern is funeral costs — not income replacement

- You've already paid off major debts and your dependents are financially independent

Choose Traditional Life Insurance If:

- You are the primary breadwinner with dependents relying on your income

- You carry a mortgage, personal debt, or other significant financial obligations

- You want to leave a larger financial legacy

- You can qualify medically and want the most coverage per dollar spent

Consider Holding Both

For some people — particularly those with an existing traditional policy — adding a final expense policy makes strategic sense. Traditional life insurance handles the larger financial picture, while a final expense policy creates a dedicated, immediately accessible fund for funeral costs so beneficiaries don't have to wait for a larger claim to process or dip into inheritance money for burial expenses.

At Vellum Life Group, clients work one-on-one with founder Eva Ikonomakos to compare both options across 10+ A-rated carriers. Many policies are approved the same day or within a few days, and the entire process is designed to be straightforward — with plain explanations and recommendations based on your actual situation, not a sales quota.

Conclusion

Neither final expense insurance nor traditional life insurance is universally the better choice. The right one depends on your age, health, financial obligations, and what your family actually needs if something happens to you.

The conversation is worth having before circumstances narrow your options. A health change, advancing age, or a major financial event can make coverage harder to get — or significantly more expensive. The time to explore is before that window closes.

If you're unsure where you stand, Vellum Life Group offers a free, no-obligation consultation to walk through both options side by side. Reach out by phone or text at 917-363-3554, email info@vellumlifegroup.com, or book a 30-minute call directly at calendly.com/eva-ikonomakos/30min.

Frequently Asked Questions

Is the $50,000 final expense benefit real?

Most final expense policies range from $5,000 to $40,000, but some carriers do offer benefits up to $50,000. Coverage limits vary by insurer, the applicant's age, and health status, so verify directly with a licensed advisor to confirm what's available for your situation.

Can someone with a pacemaker get life insurance?

A pacemaker doesn't automatically disqualify someone from life insurance. Guaranteed issue final expense policies ask no medical questions, so cardiac history is no barrier. Some traditional carriers will also underwrite pacemaker applicants depending on the underlying condition and overall health.

What is the difference between final expense insurance and whole life insurance?

Final expense insurance is technically a small whole life policy, but the purpose and scale differ significantly. Traditional whole life offers larger death benefits ($50,000–$500,000+), stronger cash value growth, and broader financial protection. Final expense is designed specifically to cover end-of-life costs affordably, with minimal underwriting requirements.

Does final expense insurance have a waiting period?

Some final expense policies — particularly guaranteed issue plans with no health questions — include a graded death benefit period of 2–3 years, during which the full payout may not apply. Simplified issue policies (where health questions are asked) often don't carry this restriction.

Can I have both final expense insurance and a traditional life insurance policy?

Yes, and for many people it's a practical combination. Traditional life insurance handles income replacement and larger financial needs, while a final expense policy keeps dedicated funds available for funeral and burial costs without drawing from the larger death benefit.

How much does final expense insurance typically cost per month?

Premiums vary based on age, gender, health, and coverage amount. For a $10,000 policy, MoneyGeek's 2026 benchmarks show costs around $30–$38/month at age 50 and $50–$66/month at age 65 for women and men respectively. Premiums are fixed for life once locked in, so applying earlier generally secures a lower rate.